Iran’s cheapest domestic car model, the Pride, has long been criticised for its poor quality and safety defects — Iranians refer to it as a “coffin on the go”.

Yet the vehicle’s position within the country’s economy has become an indicator of the financial pain facing Iranians, and the challenges for their leaders, as they vote in a June 28 emergency election after President Ebrahim Raisi was killed in a helicopter crash.

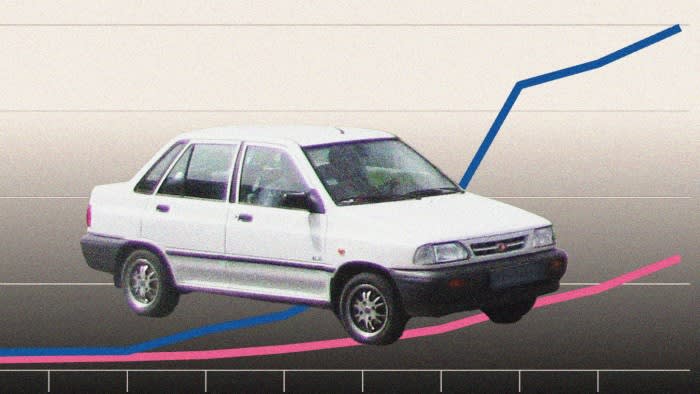

Iranians often compare the price of the Pride, a budget vehicle that carmaker Saipa began making in 1993, with the minimum wage to highlight their worsening finances. Production of what was once Iran’s most popular car ceased in 2020, but stocks remain on sale.

A decade ago a minimum-wage worker with a family of four — the minimum varies by family size — needed 1.6 times their annual income to buy a Pride; now they would need three times what they earn in a year.

Inflation and low pay have reduced living standards to a point where even the cheapest domestically produced Pride model, priced at about $6,000 on the open market, has become an unaffordable luxury for many.

For a regime accustomed to carefully choreographing political transitions, Iranians’ difficulty in affording the budget car — whose manufacturer has defended its record, but which has faced sharp criticism on safety from Iranian authorities — is one sign of why this election comes at a difficult time.

The winner will face economic problems that have intensified since 2018, when then-US president Donald Trump pulled out of the nuclear deal signed three years earlier between Tehran and world powers, and imposed waves of sanctions on the republic.

Problems facing the next leader include goods shortages and rising poverty as well as soaring inflation and a sliding currency.

Iran’s election candidates

After cracking down on dissent following waves of protests in recent years, the regime may find the election has opened up space for an unwelcome public debate.

Inflation has hovered near or above 40 per cent for years, though it has slowed slightly in recent months. That has affected every aspect of the economy.

The rate fell to single digits in the two years after Iran signed the 2015 nuclear accord with world powers, as the lifting of sanctions boosted trade, investment and tourism. But it soared close to record highs after Trump pulled out of the deal.

That jump has been widely blamed on the punitive measures, subsequent decline in oil revenues, high demand for scarce goods and the rial’s slide against the US dollar.

Iran’s authorities have also been accused of stoking price rises by printing money in the face of shrinking income from oil.

Sharply rising prices for food, housing, healthcare and transport, as wages remained low, have pushed people into poverty. More than 30 per cent of the population were living in poverty in the year to March 2022, according to the Majlis Research Center, which advises parliament.

In recent years, however, oil sales have once again become a bright spot for the leaders of the Islamic republic: oil exports rose to a six-year high in April. Iran’s GDP growth in recent years is attributed to the country selling more oil to China, its top buyer.

Iran has a relatively diversified economy but oil revenues are a critical component of GDP as well as the main source of foreign currency, making Iran vulnerable to shocks such as international sanctions.

The 2015 lifting of sanctions boosted Iran’s oil income and other exports, triggering GDP growth. But the return of sanctions on oil and banking three years later caused sharp contractions.

Tehran was later aided by the US unofficially enforcing a lighter sanctions regime on Iran, as the Biden administration polices the system less strictly than Trump.

Other important sectors such as agriculture, manufacturing, mining and services have been largely constrained by sanctions and a shortage of foreign currency reserves.

Iranians — including those who have never touched a dollar bill — frantically monitor the greenback’s open market rates to gauge their own economic prospects.

The rial has fallen sharply against the US dollar over the past decade, pushing up import prices and eroding purchasing power.

Global and regional military and political upheaval, including the Israel-Hamas war, has sent the dollar still higher, putting additional strain on the economy.

Iran’s central bank does not recognise open market rates and enforces a system of multiple exchange rates, selling cheap foreign currency to local businesses to subsidise the cost of essential imported goods.

But critics say this has resulted in profiteering, with corrupt traders selling subsidised commodities at open market rates.

Officials say subsidies on goods such as food, fuel and medicines protect ordinary people from the impact of price rises on the open market. But analysts say the public believes the subsidies are insufficient and that their expenses are inevitably shaped by dollar fluctuations.

The rial’s continued weakness has led many to convert their savings into foreign currencies as a defensive investment.

Families are hoarding between $20bn and $60bn in foreign currency cash in their homes, according to estimates by central bank officials and lawmakers.

Iranians, like people in many countries, have historically used gold as an investment to hedge against shocks such as sudden inflation, currency depreciation, war and political upheaval.

The metal is seen as retaining its worth over time and can be quickly sold in times of need or when paying for big-ticket items such as a car, home, bridal dowry or medical expenses.

It is also culturally important in Iran, with gold coins given as gifts and competition prizes. Mahr — the financial obligation undertaken by the husband to his wife at the time of marriage — is often pledged in the form of gold coins.

Families typically store their gold at home despite the risk of theft. Experts estimate Iranian households hold between 200 tonnes and 300 tonnes of the metal.

The price of a gold coin has multiplied 40 times in Iran over the past decade to the equivalent of nearly $700, a far sharper rise than that of the international gold price.

The steep increase is a double-edged phenomenon for Iranians: while gold now costs more to buy, the rise has increased the value of existing savings.

Data visualisation by Chinny Li and Keith Fray