Despite the gold prices that are almost recording levels, the prospects of the Zacks – Minderbouw – the outlook of the Golden Industry remains challenged by escalating production costs and a tight labor market. Exhausting resources, decreasing output from old mines and the extensive lead times involved in bringing new mines, together with the capital -intensive nature of such projects, indicate that industry is on its way to a delivery shortage, which ensures.

In the midst of this uncertainty, Agnico Eagle Mines ((Aem – Free report), Barrick Gold ((GOLD – Free report), Franco-Nevada Corporation ((FNV – Free report), Chinross gold ((KGC – Free report) and Alamos Gold ((AGI – Free report) have become good for growth, supported by their strong balance sheets, efforts to lower costs and growth initiatives.

About the industry

The Zacks Mining – Gold Industry mainly consists of companies that are involved in extracting gold from mines. The mines can be underground or open pits. Mining is a long and complex process and requires considerable financial resources. It is about exploring the size of a down payment; assess ways to extract and process ORTS efficiently, safely and responsible; And developing the mine before the actual mine process. It normally takes 10-20 years for a gold mine to produce material that can finally be refined. Nowadays, players in the industry use a series of advanced techniques to extract gold and convert it into Dore Bars, an alloy of gold and silver, in addition to other impurities. These are then sent for purification, after which gold is purchased as bars or coins, or used in jewelry or other purposes.

Large trends that shape the future of mining industry

Solid trend in gold prices: Spot Gold became a record high of $ 3,059 per ounce after the announcement of US President Donald Trump of new car rates. Gold has remained above $ 3,000 per ounce since mid -March, driven by the demand for safe port in the midst of geopolitical and economic uncertainties. The imposition of American rates and fears for an escalating trade war also struck prizes. This year, the Federal Reserve indicated the possibility of two interest rates. Gold has won 16.3% so far and this trend will probably continue to exist, supported by buying central bank and global tensions. However, the attention of investors is now aimed at the most important economic data, such as the price index of the Personal Consumption Expenditures (PCE), the preferred infection meter of the FED, which could offer further indications for monetary policy.

High costs, labor shortages are worrying: The industry has confronted with a shortage of competent workforce, which causes a peak in wages. Industrial players are constantly struggling with escalating production costs, including electricity, water and material and supply chain problems. Since the industry cannot control gold prices, it focuses on improving the sales volume and the operational cash flow and reducing the net cash costs. The participants in the industry opt for alternative energy sources, such as solar energy or wind farms, to minimize the volatility of the fuel price and the secure range. Miners are committed to cost reduction strategies and digital innovation to stimulate operational efficiency.

Declining delivery of a care for the industry: Exhausting agents, decreasing delivery in old mines and the lack of new mines have been an eternal problem for industry. Due to the scarcity of discoveries and exhausting existing resources, miners prefer to build up reserves via acquisitions instead of digging new that are risky and capital -intensive. On the demand side, the use of gold in energy, health care and technology is increasing. India and China account for around 50% of consumer gold demand. The yellow metal has long been considered a safe port investment in financial or political uncertainty. The demand of the gold continues to increase from central banks. That is why there will be any imbalance of the question delivery.

Zacks Industry Rank indicates boring prospects

The Zacks Industry rank of the group, in fact the average of the Zacks rang of all memberships, indicates gloomy prospects in the short term. The Zacks Mining -Gold Industry, a 39 -stock group within the wider Zacks Basic Materials sector, currently has a Zacks -Industrierang #153, which places it 38% of 246 Zacks Industries at the bottom.

Our research shows that the top 50% of the Zacks-ranked industries performs the bottom 50% better with a factor of more than 2 to 1.

Before we present a few shares that you may want to consider for your portfolio, let’s look at the recent performance and the valuation photo of the industry.

Industry versus S&P 500 & Sector

The mining industry has performed the S&P 500 index and the basic material sector better in a year. The shares in the industry jointly won 43.7% against the decrease in the wider sector of 3.9%. The S&P 500 has risen by 10.7% in the same time frame.

A year of price performance

The current appreciation of the industry

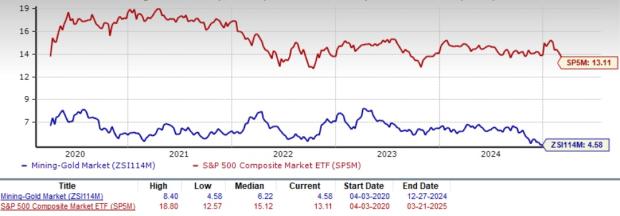

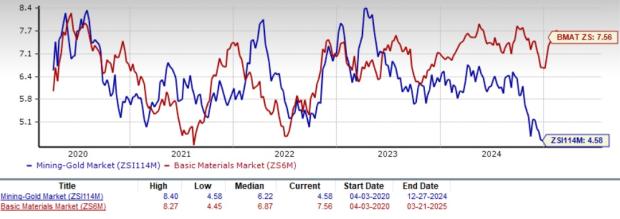

Based on the forward 12-months EV/EBITDA, a generally used several for the appreciation of gold mining companies, we see that the industry is currently trading at 4.58x compared to the 13.11x of the S&P 500 and the Voorwartse 12-month EV/EBITDA of 7.56X of the graphs. This is displayed in the graphs.

Enterprise value/EBITDA (EV/EBITDA) F12M ratio

Enterprise value/EBITDA (EV/EBITDA) F12M ratio

In the past five years, the industry was exchanged as high as 8.40 times and as low as 4.58 times, with the median 6.22x.

5 Mining-gold shares to keep an eye on

Agnico Eagle Mines: The company recently closed the acquisition of O3 -Mijnbouw and owns the Marban Alliance real estate. The integration of this real estate with the Canadian Malartic Land package of the AEM will create important and unique synergies. The company’s focus remains on extending the mining life in existing activities, testing near-my opportunities and promoting the most important value of the most important value of the driver. Exploration priorities for 2025 include conversion and expansion of mineral resources in the Detour Lake Underground project and East Gouldie at Canadian Malartic, as well as Advancing Hope Bay. AEM has succeeded in reducing the costs by optimizing the drilling of productivity and innovation efforts. The efforts to reduce debts are also commendable.

The Zacks Consensus estimate for the income from the Gold Mining Company of Toronto, Canada, in 2025 in Canada, indicates an annual basis of 6.4%. AEM has on average a backlog of a four -quarter win of 16.4%. The company has an estimated profit growth in the long term of 31.6%. Agnico Eagle Mines currently has a Zacks rang of 3.

Price and consensus: AEM

Barrick Gold: The company is well placed to take advantage of the progress in important growth projects that should considerably stimulate production. The most important growth projects for gold and copper, including Goldrush, the expansion of the Pueblo Viejo factory and my life extension, Donlin Gold, Fourmile, Lumwana Super Pit and Reko DIQ are currently executed. These projects are based on schedule and within the budget, underlie the next generation of profitable production. Barrick has a solid liquidity position and generates healthy cash flows, which positions it well to take advantage of attractive development, exploration and acquisition possibilities, to stimulate shareholder value and reduce the debts.

The Zacks Consensus estimate for the income of Toronto, Canada in Canada in the Tax 2025 indicates a growth of 8% on an annual basis. Gold has on average a backlog of a four -quarter win of 12%. The company currently has a Zacks rang of 3 and an estimated profit growth in the long term of 11.4%.

Price and consensus: gold

Franco-Nevada: FNV appears on a promising long-term trajectory, supported by a healthy portfolio of streaming and royalty agreements on various property mined by some of the most renowned mining companies in the world. It expects the total geos to be between 465,000 and 525,000 in 2025, indicating an increase of 7% on an annual basis at the center. Given the focus on cost management, FNV has generated high margins. The company is debt -free and uses its free cash flow to expand the portfolio and to pay dividends. On February 28, 2025, Franco-Nevada acquired a precious metal metal stream from the South African mines of Sibanye-Still water for $ 500 million, which expected more than 45 years of deliveries, usually gold and platinum, with initial deliveries of around 27,000 geos.

The Zacks Consensus estimate for this income of gold-oriented royalty and streaming company from Toronto, Canada, indicates a growth of 15.9% on an annual basis. FNV has on average a four -quarter backlog in profit surprise of 2.8%. The company has an estimated profit growth in the long term of 3.6% and currently has a Zacks rang of 3.

Price and consensus: FNV

Chinross gold: The strong liquidity position and substantial cash flows of the company enable it to finance its development projects, while paying on debts and stimulating shareholders’ value. Kinross Gold has a strong production profile and has a promising pipeline of exploration and development projects. The most important development projects and exploration programs, including Great Bear in Ontario, the Redbird Pit in Bald Mountain and Round Mountain phase X in Nevada, remain on the right track. These projects are expected to stimulate production and cash flow and provide considerable value.

The Zacks Consensus estimate for the income of this Gold Mining Company from Toronto, Canada, for Fiscal 2025, indicates 14.7% on annual basis growth. KGC has on average a lagging square profit surprise of 23.7%. Kinross Gold has an estimated profit growth in the long term of 21% and a Zacks rang of 3.

Price and consensus: KGC

Alamos Gold: The company projects the production from 24% to 680,000-730,000 Ounces in 2027, powered by Island Gold District, Young Davidson and Mulatos. Verwacht wordt dat all-in-bestaande kosten (AISC) met 8% zullen dalen ten opzichte van dat tijdsbestek van die gerapporteerd in 2024, vanwege de goedkope groei van eilandgoud na de voltooiing van de fase 3+ uitbreiding in de eerste helft van 2026. AGI kondigde een bouwbeslissing aan het Lynn Lake-project in januari 2025, met de eerste helft van de helft van de helft van de helft van 2028. Speel een belangrijke rol When bringing the company’s production to around 900,000 ounces per year (with an annual growth of 59% from 2024).

The estimate of the Zacks consensus for the income of Toronto, Canada in Canada, indicates an increase of 41.2% on an annual basis. AGI has a long -term profit growth of 10.1%. On average, it has a four -quarter surprise of 7.9%. Agi currently has a Zacks rang of 3.

Price and consensus: Agi